At least three of the artists involved are not on simple, straight-up deals with major record companies. Drake and Future’s “Life Is Good” is signed to Sony’s Epic, but via Future’s own label, Freebandz; Nicki Minaj’s “Yikes” is claimed by Universal’s Republic Records, but via both Cash Money and Young Money — the latter being the imprint founded by Lil Wayne in 2007; Justin Bieber’s “Intentions” is out on another Universal label, Def Jam, but in tandem with Raymond-Braun Media Group (RBMG), the label co-owned by Bieber’s manager, Scooter Braun, and Usher.

Without seeing the contracts of each of these artists, we can’t know the exact nature of their record deals. But we do know this: Such additions and caveats speak volumes about a modern music industry where artists (and/or their representatives) are getting paid a bigger cut of royalties than ever — and are giving away their rights for shorter durations.

To date, the apotheosis of this story has come from Taylor Swift, who confirmed that in her deal with Universal/Republic Records she outright owns the masters for Lover and its expected successors. (Universal is either providing marketing and distribution services to Swift on a work-for-hire basis, or, more likely, she’s signed a short-term licensing deal for Lover, after which full control of her rights will land back in her grasp.)

As recently as 20 years ago — when physical goods still ruled the music industry and when breaking through on radio was your only real shot at success in the States — record labels typically offered a contract whereby the artist got an upfront check, but the label got lifetime ownership of rights and 80-plus percent of royalties. These days, that’s all changed: A more typical major deal with an established star (or even a fast-rising new independent talent) will see rights ownership revert back to the artist much sooner, with a baseline 50/50 (profit share) royalty deal. Increasingly, for global megastars, major labels are actually agreeing to a minority of royalties.

If major labels do want to achieve a 50 percent or upward royalty level — let alone license rights for a decade-plus — they have to pay stars an eye-watering amount for the privilege. As Sony Music Group chairman and CEO Rob Stringer said at a Goldman Sachs conference last September: “It’s much more expensive today to sign talent than it was six months ago, and it’s way more expensive than two years ago — and going back to the 2000s, the download era, it’s not even comparable.”

Stringer added: “It’s a balancing act between how much we spend on talent and how much we get back [in terms of percent of royalties and licensing length]. That’s always been the adage, but the mathematical formula is a little bit more complicated now.”

This transformation, driven by the artist-empowering explosion of Spotify, SoundCloud, et al., plus the natural erosion of traditional media’s influence, is a potential future danger for the majors, should they not counter against it. And at least one of their ranks, as demonstrated below, is keeping a smaller portion of the money it generates each year, as the artists’ share continues to swell.

Love Music?

Get your daily dose of everything happening in Australian/New Zealand music and globally.

Earlier this month, Warner Music Group shocked the industry by announcing its intention to go public on the New York Stock Exchange, in a move that will see owner Len Blavatnik attain a company valuation many multiples higher than the $3.3 billion he paid for WMG in 2011. (Well, I say “shocked the music industry,” but a month ago, in Rolling Stone, I predicted that Blavatnik would cash in a minority stake in WMG this year. I also predicted Tencent might do the buying; if WMG does land on the stock market, let’s see if the Chinese company makes an institutional acquisition of shares.)

Warner announced its IPO on February 6th, via a standard S-1 form filed with the SEC that revealed pretty much everything about the company’s fiscal performance over the past few years. (It’s all in there: risk factors, revenue rises, management salaries, profit figures — the works.)

Yet there’s one essential statistic that this document doesn’t make much noise about. And, for my money — quite literally — it’s the single most important data point would-be investors in WMG should be focusing on.

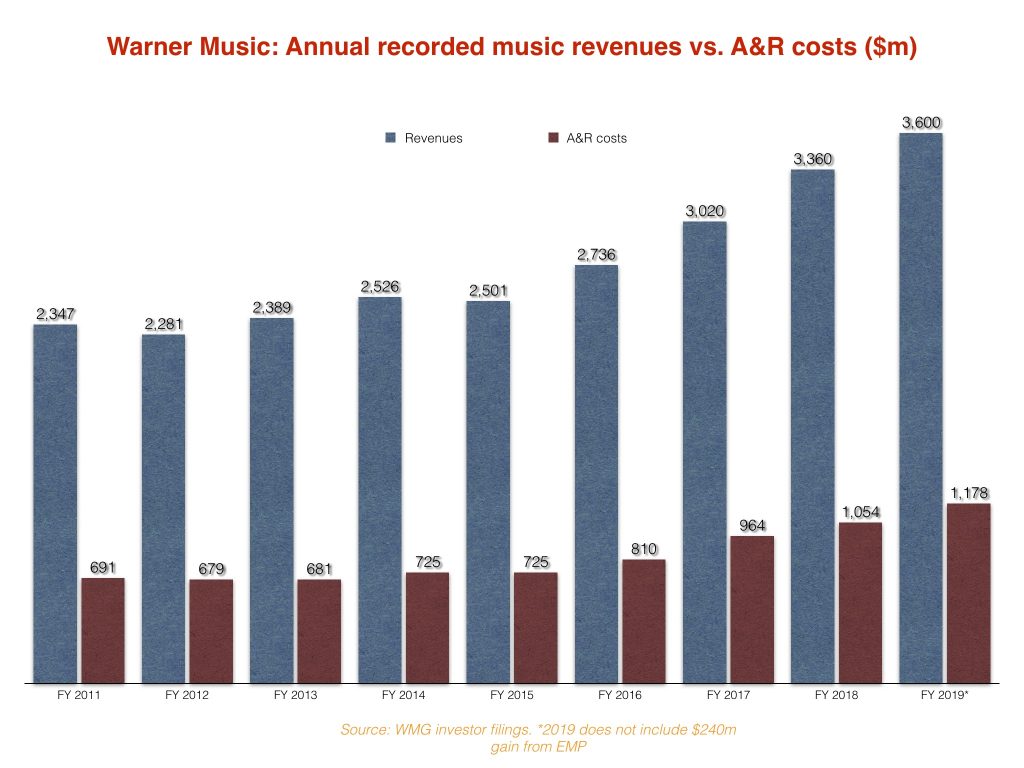

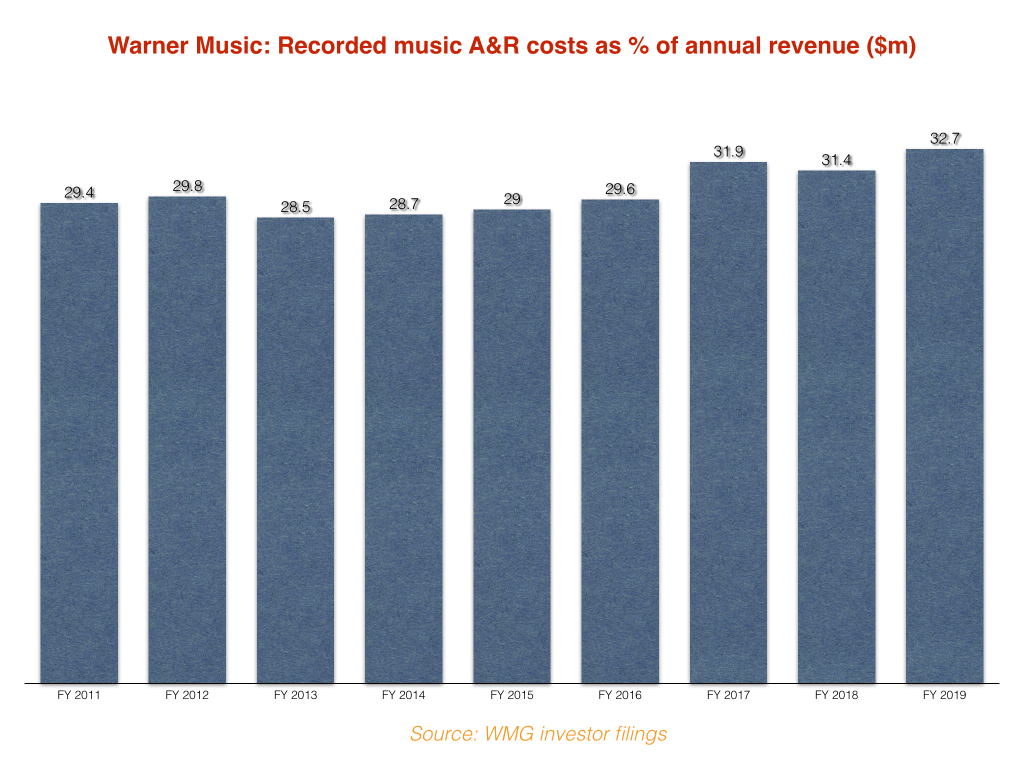

Below, you can see the annual figures for Warner’s recorded-music revenues, alongside what the firm calls in financial documents its “Artist and Repertoire costs.” These A&R costs, says Warner, cover any company expenses associated with “(i) paying royalties to recording artists, producers, songwriters, other copyright holders, and trade unions; (ii) signing and developing recording artists; and (iii) creating master recordings in the studio.”

In other words, it’s a combination of the royalties Warner is paying out to artists, plus advance checks its labels are signing, plus — making up the minority of the money — the cash it needs to enable a star to make magic in the studio.

This A&R costs figure is therefore a fascinating indicator of the underlying economics of today’s record deals, i.e., how generous major labels are being forced to be with their funds.

(Three quick notes on this: 1. The most important graph here is the second, which shows the percentage of Warner’s total annual recorded-music revenues that were eaten in each year by A&R costs; 2. In both graphs, I have removed $240 million from Warner’s fiscal year 2019 revenue figure, as, according to WMG, this was the annual sales rise triggered by its $180 million acquisition of EMP, a European merchandise and online sales store, in October 2018. Removing this number from the revenue line gives us a true like-for-like, year-on-year comparison; 3. Warner’s fiscal year closes at the end of September, if you were wondering.)

Over the past five years, the percentage of recorded-music revenue Warner has spent on A&R costs (mainly, on artist royalties and advances) has shot up, from 28.7 percent in fiscal year 2014 to a new high of 32.7 percent in fiscal year 2019 (+ four percent).

To put this into context, every one percent you see in the bar above for FY 2019 is equivalent to $36 million — money that would otherwise have gone straight to Warner’s bottom line. Had that 32.7 percent in 2019 remained at 28.7 percent, it would have saved Warner Music Group $144 million last year.

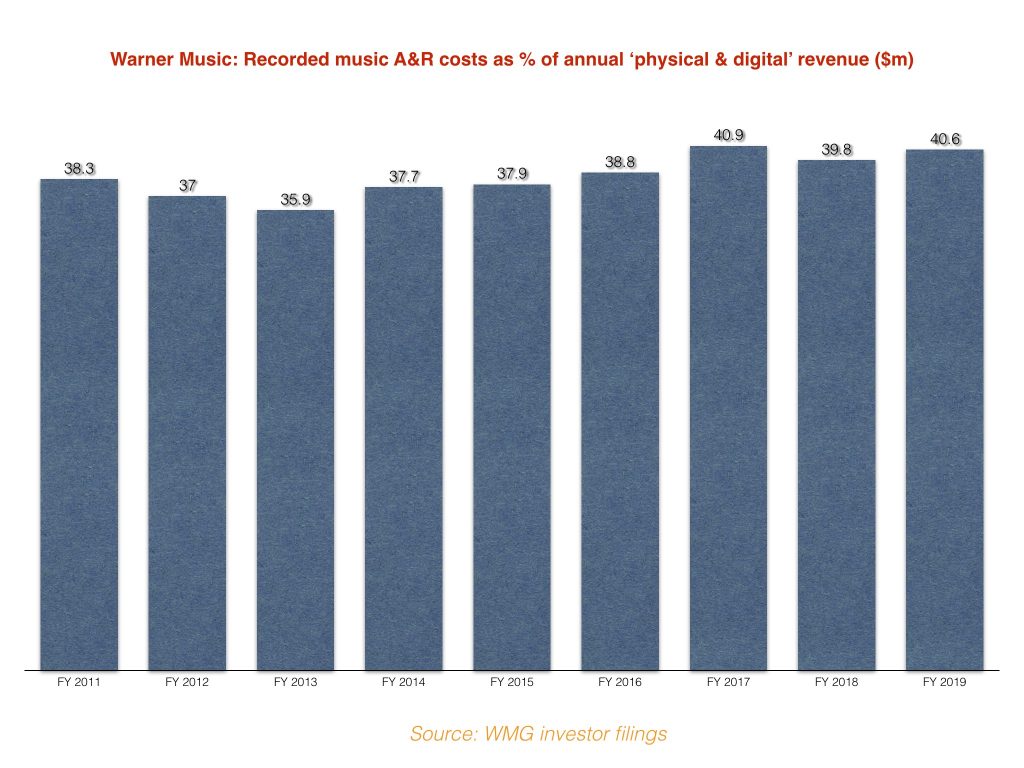

Delving deeper into Warner’s numbers, there is an even more telling indication of how rising artist costs could cause investors issues in years to come. Within its SEC filings, WMG’s recorded-music revenues are broken down into three constituent parts: Licensing; Artist Services & Expanded Rights; and Total Physical & Digital.

The latter category is Warner’s core business — every penny that flows through to the firm from Spotify, Apple Music, YouTube, etc., plus music retail stores across the world, is covered here. (The EMP money is categorized under “Artist Services” by the way, which also covers Warner’s participation in live-music ticket sales.)

The trend continues: Twice in the past three years, Warner has shelled out more than 40 percent of the money it accrues annually from its core recorded-music business to pay artists.

The question for Warner’s IPO watchers, then, is: What happens when this 40 percent figure rises to 45 percent, or above 50 percent, in the future?

The cost of modern deals will be the key factor pushing this annual number upward. Consider that artists signed back in the Seventies or Eighties often bemoan enduring major-label royalty contracts from that era that give them 18 percent or less of the spoils from streaming today — and even, unbelievably, sometimes see extra money removed from their pay packets for the laughably outmoded “packaging deductions.” (This is a very serious issue for certain acts. When I spoke to Squeeze singer-songwriter Glenn Tilbrook for this column at the end of last year, he took my breath away with this quote: “This is a harsh comparison, but I make it freely: [In terms of] the deal we signed when we were kids, it’s like I see a direct relation between pedophiles and record companies, in that they have the same predatory instincts and ability to charm and outwit people who are easy to outwit.… That whole end of the business is shoddy, manipulative, and coercive, and it’s not nice.”)

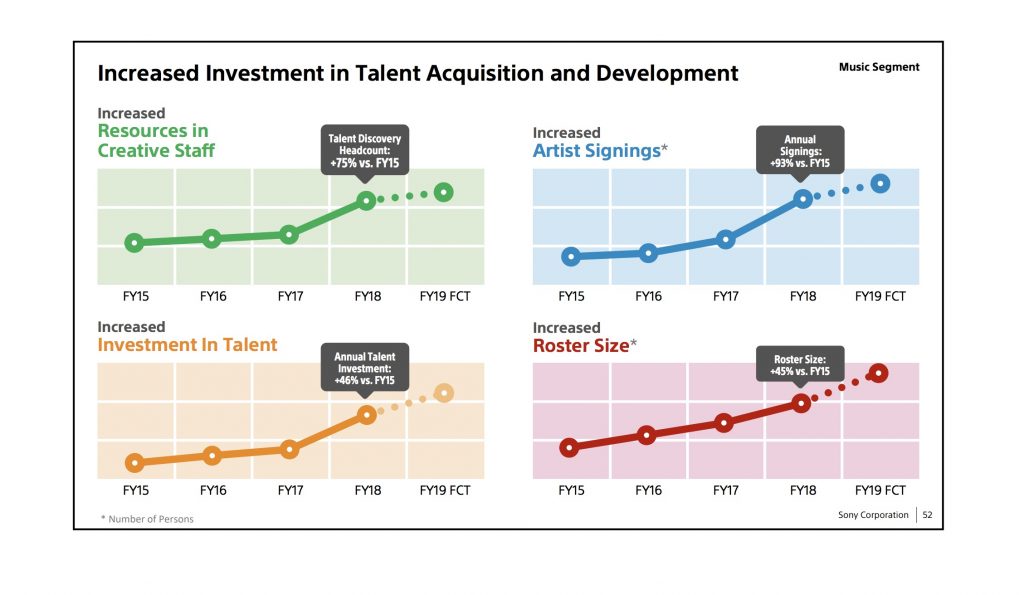

The rapidly rising spending on artists at major record companies is most definitely not solely a Warner phenomenon. In a presentation given to Sony at its investor day last year (pictured below), it was revealed that Sony Music’s annual expenditure on signing and developing artists had risen by 46 percent in FY 2018 compared with FY 2015. Indeed, according to scarcely believable IFPI stats, the majors were actually spending $11 million a day on A&R in 2017 — a number that will have only escalated since.

For now, Warner’s owners don’t need to be too worried about the ever-creeping percentage of revenues being spent on talent because, in monetary terms, the company’s growth is more than keeping pace. For example, between FY 2015 and FY 2019, the annual amount spent on A&R by Warner’s labels grew by $453 million — but the amount of total recorded-music revenue coming into the company per year grew by more than double that figure, at $1.01 billion. Spending more on artists when your top-line revenue is soaring obviously isn’t a problem — but it will become one if the growth of global streaming tails off. And, as regular readers of this column know well, that’s exactly what’s beginning to happen across the industry today.

To some extent, major labels can safeguard against this trend by diversifying their income streams beyond pure recorded-music royalties (Warner’s EMP buy looks extra-smart in this context). Yet the fact remains, Warner – as well as Universal Music Group, which announced its own intention to IPO this week – is now opening itself up to the stock market on the cusp of an era when a global streaming-growth slowdown seems inevitable, and is only getting more pronounced.

As such, Len Blavatnik’s management team may wish to brace itself for some difficult post-IPO questions from investors regarding the amount of money WMG is spending on artists — and whether, in an unwelcome scenario for any creative business, there’s any chance it could cut back.

Tim Ingham is the founder and publisher of Music Business Worldwide, which has serviced the global industry with news, analysis, and jobs since 2015. He writes a weekly column for “Rolling Stone.”